Kinds of Cash Books: Simple, Two Column, Three Column, Petty etc

A cash book is a subsidiary book that includes both cash and bank transactions, and it is a journal and a ledger. Some companies utilize cash books instead of cash receipts journals and cash payments journals. Since all cash receipts and payments are recorded in cash books, it is easier to access information.

Double Entry Bookkeeping

The cash book may become very bulky and the cashier may be overburdened. Applying the rule of ‘management by exception’ the main cashier should not be disturbed for small and petty items. Every business organization, whether a small entity or a large company, needs to maintain and prepare the records of its daily transactions. The format of a single-column cash book will be something like this. Because the cash book acts as both; in the journal and ledger, the closing balance of it is directly transferred to the trial balance.

Receipt of Cheque or Cash

There is no requirement to transfer the balances to the general ledger, which is required in the case of the cash account. There are numerous reasons why a business might record transactions using a cash book instead of a cash account. Mistakes can be detected easily through verification, and entries are kept up to date, as the balance is verified daily. By contrast, balances in cash accounts are commonly reconciled at the end of the month after the issuance of the monthly bank statement.

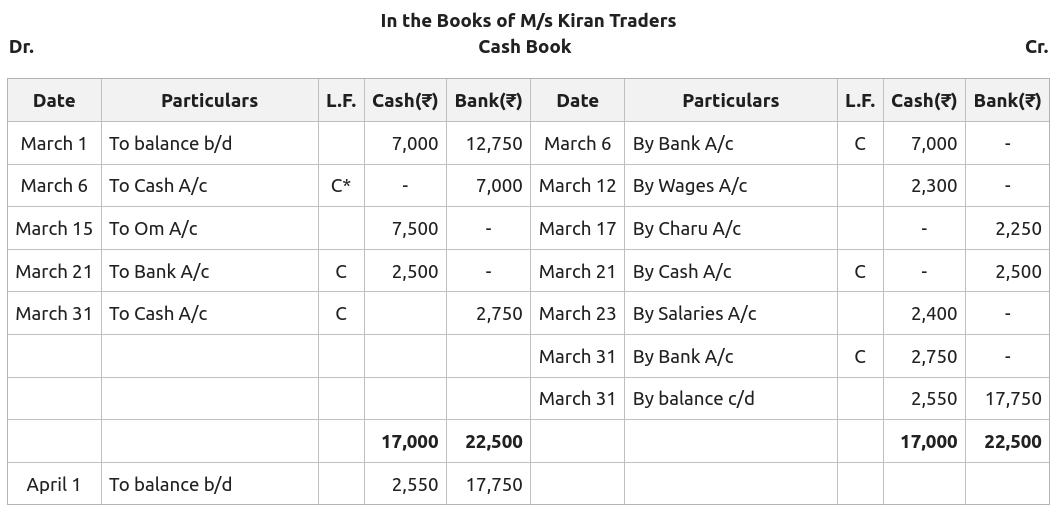

Sample Format of Two Column Cash Book

‘L.F.’ column shows where the posting of these items have been made in respective ledgers. The small cash transactions taking place a significant number of times daily if recorded in a general cash book may make it bulky and difficult to handle. A cash book has simplified the entry cash transactions for accounting purpose to a great extent. As it is maintained date wise, any cash payments or the transaction can be correctly traced back in the cash book. Cash book is a special type of book that is only concerned with the recording of cash transactions of an organisation. It performs the dual role of both journal and a ledger for all the cash transactions taking place in a business organisation.

- As such, the single-column cash book provides less detailed information than the double-column cash book.

- Since all cash transactions are recorded in this book in the ledger account format, a separate cash account in the ledger is not needed.

- Since it can be encashed over the counter, there’s less control over who can access the funds, which increases the risk.

- They allow businesses to keep track of payments and receipts in a detailed way.

- The cash book may become very bulky and the cashier may be overburdened.

Accounting Ratios

On the credit side, however, debit transactions are reflected as deductions and are exponentially updated as your list builds up. In one sentence, a cash book is a basic accounting document used for recording deposits and withdraws. The triple-column cash book has three columns for recording cash, bank, discount received and discount given. It records the cash transactions and works as a book of original entries and ledger. A cash book is a record of the cash transactions of the business. The main purpose of the cash book is the effective management of cash.

Record the following transactions in a simple petty cash book for the month of January 2019. A petty cash book is maintained to record small expenses such as postage, stationery, and telegrams. Record the transactions shown below in a single column cash book and post to the ledger.

In this way, the petty cashier will begin every period with an amount equal to imprest cash, and the amount held by the petty cashier will never exceed this. The amount spent by the petty cashier is reimbursed, thus making up the balance to the original amount. At the end of the period, the petty cashier submits the statements covering petty expenditures to the chief cashier.

There is one on each side for recording discounts, cash, and bank amounts. One column shows cash receipts and payments, the second records banking transactions, and the invoice online or on the go third notes discounts received and allowed. Keeping records of business transactions is crucial, so properly maintaining the books helps businesses run smoothly.